Newsletters

Newsletters

U.S.-based investment bank Goldman Sachs forecasted that the Central Bank of the Republic of Türkiye (CBRT) may raise its key interest rate by as much as 350 basis points, either during its next scheduled Monetary Policy Committee (MPC) meeting on April 17 or even before that date.

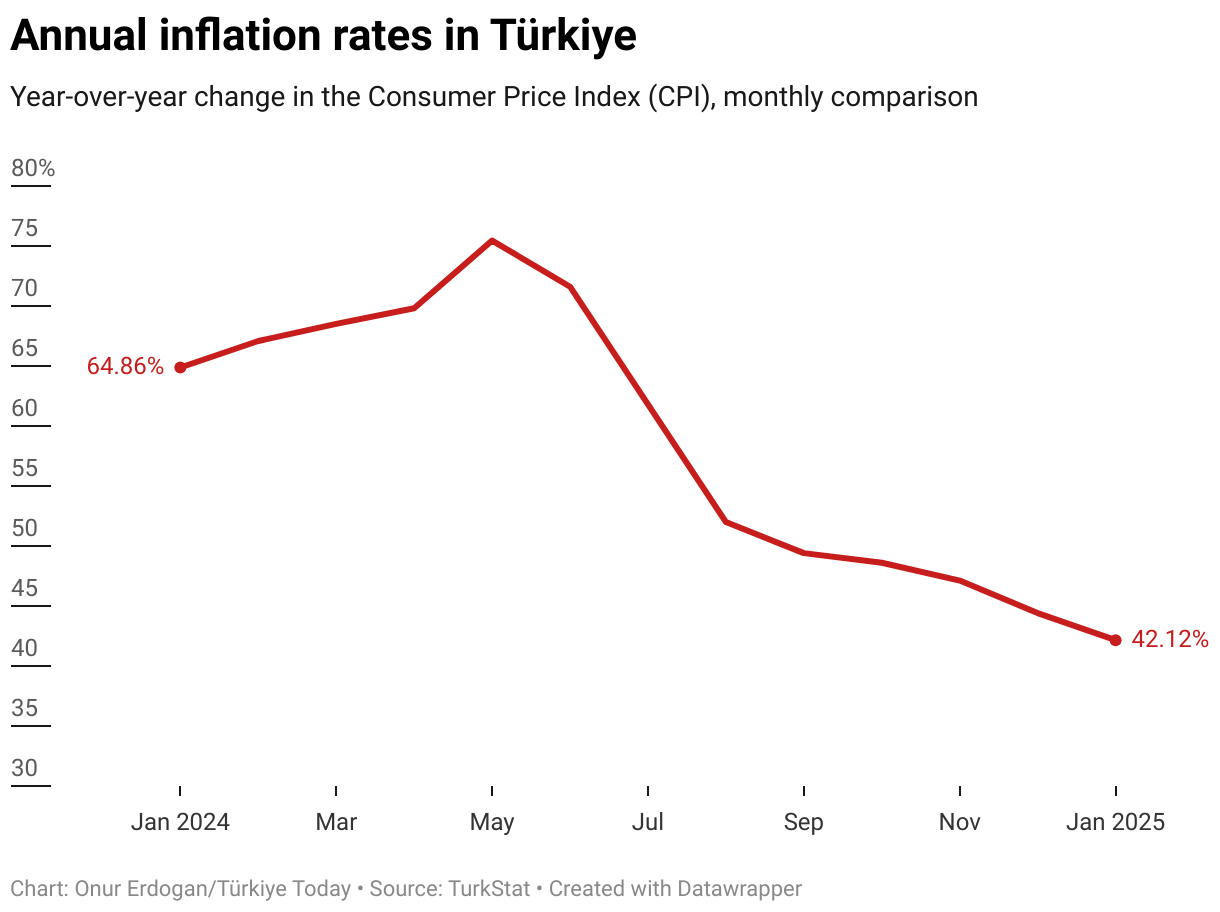

Turkish central bank reduced the policy interest rate to 42.5% by a 250-basis points cut in its latest MPC meeting on March 6, following February's better-than-expected inflation figures at 39.05%, reported by the Turkish Statistical Institute (TurkStat).

| MPC meeting | Policy rate (%) |

|---|---|

| 07.03.2025 | 42.50 |

| 24.01.2025 | 45.00 |

| 27.12.2024 | 47.50 |

| 22.03.2024 | 50.00 |

| 26.01.2024 | 45.00 |

The report also sheds light on the CBRT’s abrupt move on March 20, when it raised its overnight lending rate by 200 basis points. This step, according to Goldman Sachs, was taken in response to increasing market volatility and was intended as a temporary measure to calm investor nerves while giving the central bank more time to assess conditions and communicate with stakeholders before considering changes to the policy rate.

Economists believe the decision reflected both a sense of urgency and a desire for more coordinated policymaking.

Goldman Sachs further identified a major underlying risk to the central bank’s strategy: the potential return of “dollarization”—a process where domestic savers shift their deposits from Turkish lira to foreign currencies, especially the U.S. dollar.

This often occurs in economies where confidence in the local currency is low, particularly during periods of high inflation or political uncertainty.

If dollarization gains momentum again, the report warned, it could seriously undermine the effectiveness of monetary policy by reducing the CBRT’s control over the money supply and weakening the impact of interest rate hikes. It could also derail efforts to stabilize inflation and lead to renewed exchange rate pressures.

Despite these risks, the Goldman Sachs report expressed cautious optimism, arguing that Türkiye’s relatively strong foreign exchange reserves could help buffer the impact of capital outflows and market sell-offs and that the central bank still has room to maneuver—provided it acts decisively and maintains transparent communication with investors.

1 min read

1 min read